[ad_1]

Genco Shipping & Trading (NYSE:GNK) is a dry bulk shipping company. Dry bulk shipping has gone through a monster bear market. This makes it an interesting place to look for value.

A number of investment firms own large blocks of shares of Genco: Apollo Global Management (15.7%), Centerbridge Partners L.P. (30.4%) and Strategic Value Partners LLC (29.4%). The company issued a set of shares earlier this year at a higher price and expanded its fleet. Management also expressed the desire to sell ships. This seems contradictory, but shipping is an ongoing fight against time. The fleet has to be rejuvenated constantly. Executives manage that by buying and selling ships opportunistically.

The CEO has investment banking experience, which is helpful if you are building a company. It does come with a price tag, as executive compensation seems high. It looks like the strategy is to scale up the business. If we are really coming out of the dry bulk bear market, that will work out great.

The market doesn’t seem to care for the plan, as the stock has sold off sharply since mid-year:

GNK data by YCharts

GNK data by YCharts

Earnings estimates have been revised upwards recently, and we’re looking at a ~5.5x forward earnings multiple. Don’t take earnings estimates for shipping companies that are more than a few months out too seriously. In my view, it’s more important to review the assets. The assets are your downside protection. For upside, we’ll just have to sit back and see what it’s going to be. However, EPS estimates do show that there can be a lot of upside.

GNK EPS Estimates for Next Fiscal Year data by YCharts

GNK EPS Estimates for Next Fiscal Year data by YCharts

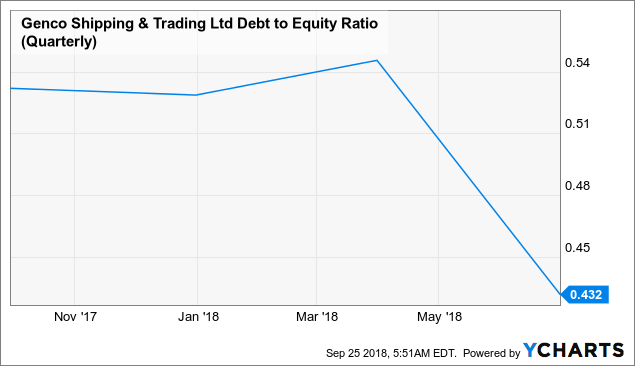

To get back to the subject of downside protection, the debt-to-equity ratio is important. It sits at a very reasonable 0.43x. That’s even more reasonable if you take into account shares have been near $20 earlier in the year. Just a few months ago, on June 15, Genco sold 7 million shares at $16.5, or $3 higher per share, supposedly to knowledgeable buyers.

GNK Debt to Equity Ratio (Quarterly) data by YCharts

GNK Debt to Equity Ratio (Quarterly) data by YCharts

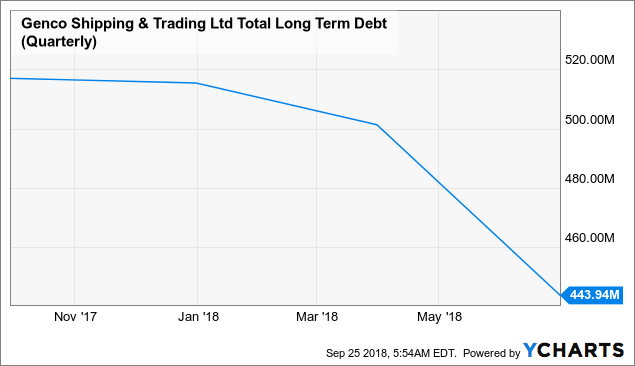

More worrying is the company’s debt-to-EBITDA ratio, which exceeds thirty. I’ve broken it out into absolute numbers. With some perspective, it becomes more digestable. The total long-term debt is around $443 million:

GNK Total Long Term Debt (Quarterly) data by YCharts

GNK Total Long Term Debt (Quarterly) data by YCharts

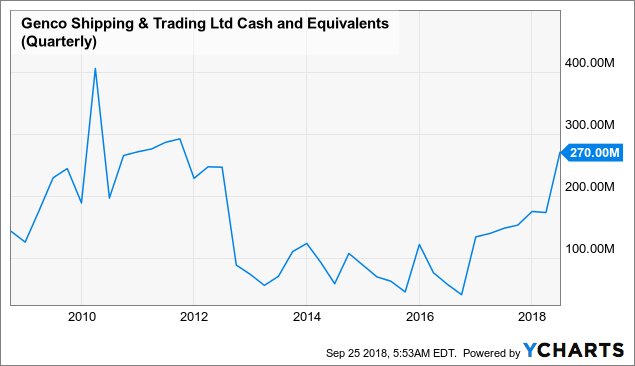

There’s also a large amount of cash that can be used for a variety of purposes. Part should be kept to remain compliant with debt covenants, which require a certain liquidity, and as a buffer against disappointments. The cash hoard is so large that it will likely be put to better use, like towards: 1) buying ships, 2) extinguishing debt, or 3) buybacks (very unlikely).

GNK Cash and Equivalents (Quarterly) data by YCharts

GNK Cash and Equivalents (Quarterly) data by YCharts

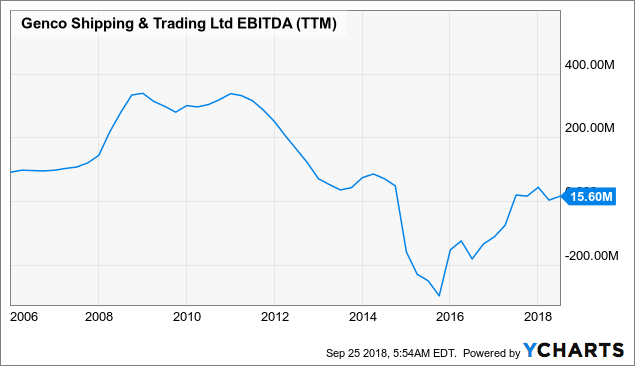

$15 million in EBITDA pales in comparison to the debt load. Even at a net debt of $170 million, that’s still 12 times EBITDA. Companies with extremely steady revenue can afford to lever up to 6x.

Shipping is not a business with predictable revenue at all. Yet, as the graph below shows, Genco’s EBITDA has swung wildly all over the place. It has been much higher in the past on a smaller asset base.

Importantly, the company didn’t take possession of some of its acquired ships. As these enter service, they start contributing to EBITDA, and it should improve. Meanwhile, the debt is already there, as the money has been spent.

GNK EBITDA (TTM) data by YCharts

GNK EBITDA (TTM) data by YCharts

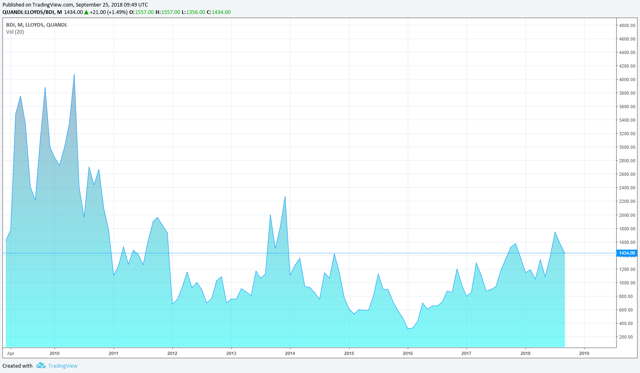

With ships entering the fleet and ample liquidity on the balance sheet, I’m not as worried about the high EBITDA multiple. If you look at this graph of dry bulk rates, we aren’t at an all-time low. Rates could definitely improve, as demonstrated by the peak in 2010.

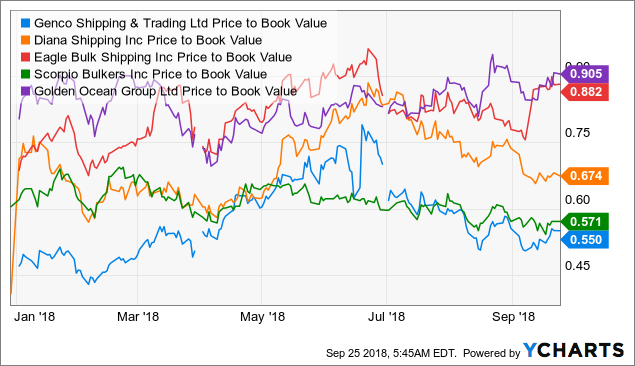

If I put Genco’s price-to-book value in context of those of dry bulk competitors like Diana Shipping (NYSE:DSX), Eagle Bulk Shipping (NASDAQ:EGLE), Scorpio Bulkers (NYSE:SALT) and Golden Ocean Group (NASDAQ:GOGL), it is trading at the lowest multiple among all of them:

GNK Price to Book Value data by YCharts

GNK Price to Book Value data by YCharts

Conclusion

Most names in the space look fairly attractive to me compared to the general S&P 500 company. Genco is even more so. I like the plan of scaling up through opportunistic buying. I like the shareholder base. I like the fact that the company raised money at higher prices. The liquidity situation still looks very healthy. I also like the relative value. I’d be very surprised if I look back at this in five years and it didn’t make money.

Check out the Special Situation Investing report if you are interested in uncorrelated returns. We look at special situations like spin-offs, share repurchases, rights offerings, M&A events, etc. But we also have a keen interest in the commodity space. Especially in the current late stages of the economic cycle.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

[ad_2]

Source link Google News