[ad_1]

In our column two weeks ago we took a first look at the Governor’s proposed FY23 10-year Plan (FY23 10-Year Plan), concluding that it was not sustainable on its face and once we looked deeper, also not realistic on the spending side. Based on that, last week we made the adjustments necessary to incorporate more realistic spending levels, concluding that, even after taking into account all of Governor Mike Dunleavy’s (R – Alaska) proposed adjustments, including the administration’s proposed spending reductions, the budget realistically remains about $500 million per year in deficit over the 10-year period.

This week, we look deeper into the alternatives for closing those deficits, the potential impact of those alternatives on Alaska families and, through them, the overall Alaska economy.

As we noted in our initial look at the FY23 10-Year Plan, by using a combination of higher oil prices and federal funds Dunleavy’s FY23 budget creates “a bridge” period before again plunging into deficits beginning in FY24. But renewed deficits are coming quickly and will need to be dealt with one way or another.

Advertisement. For information about purchasing ads, please click here.

As we explain in this column, some alternatives have a much lower adverse impact on Alaska families and the overall Alaska economy than others, but they will take some time and effort to put in place. The FY23 “bridge” provides the opportunity to do the work necessary to put them in place before reaching the other side.

The Baseline

As a baseline, we start with the impact of the Governor’s own proposed revenue raiser embedded in his budget. In order to move as far as his 10-year Plan does toward a balanced budget the Governor proposes to restructure the PFD from the current statutory approach to POMV 50/50. As we explained last week, due to the differences between the two approaches in accounting for the inflation adjustment, that’s an average reduction from the current law PFD (and shift to government revenues) of about $600 million annually over the next 10 years.

As the University of Alaska-Anchorage’s Institute of Social and Economic Research explained in a 2017 report assessing the impact of various fiscal options on Alaska families, of all the various revenue options PFD cuts are “by far the costliest measure for Alaska families.” Because “[t]he impact of the PFD cut falls almost exclusively on residents, and it is highly regressive,” ISER also concluded in its 2016 report on Alaska’s Fiscal Options (ISER 2016 Report) that the approach has “the largest adverse impact on the economy per dollar of revenues raised” of the various options it reviewed.

Despite those negative impacts, the Governor’s budget nevertheless adopts the option as part of the Administration’s base FY23 budget and 10-Year Plan. This chart, based on the 2017 distributional analysis done for the legislature by the Institute on Taxation and Economic Policy (ITEP 2017 Report), demonstrates the impact of that decision on Alaska families compared to current law by income bracket.

In Diapering the Devil (available online here as Chapter 2 of “The Governor’s Solution”), Governor Hammond called PFD cuts “a reversibly graduated head tax.” Applying that definition, Governor Dunleavy’s proposed restructuring effectively adopts baseline tax rates (expressed as a share of income) starting in FY23 of 0.2% on the top 1% of Alaska families, 3% on middle income Alaska families and 8.6% on the lowest 20% of Alaska families.

Advertisement. For information about purchasing ads, please click here.

As is apparent, compared to current law the Governor’s proposed revenue raiser is hugely regressive, taking 43 times more from low, and 15 times more from middle income Alaska families than from the top 1%.

Major Alternatives for Closing the Remaining $500 Million Gap

As we explained in last week’s column, we believe the level of additional revenues above those projected in the Governor’s FY23 10-year Plan required to achieve a sustainable budget on the other side of the FY23 “bridge” is in the range of $500 million per year, the average of the projected deficit levels from FY24 through FY30 using a 2.5% inflation factor.

Over time, various alternatives have been proposed for closing the remaining gap. Below, we look at the impact of the three – deeper PFD cuts, sales taxes and an income tax – that historically have received the most attention.

For each, we show the cumulative effect of stacking them on top of the Governor’s baseline proposal. Some propose to look at the alternatives instead on a stand-alone basis, treating the Governor’s proposed baseline PFD restructuring essentially as a sunk cost. To us, however, that piecemeal approach has the effect of seriously understating the full impact of the proposed measures on Alaska families, particularly on middle and lower income Alaska families who bear the brunt of the impact.

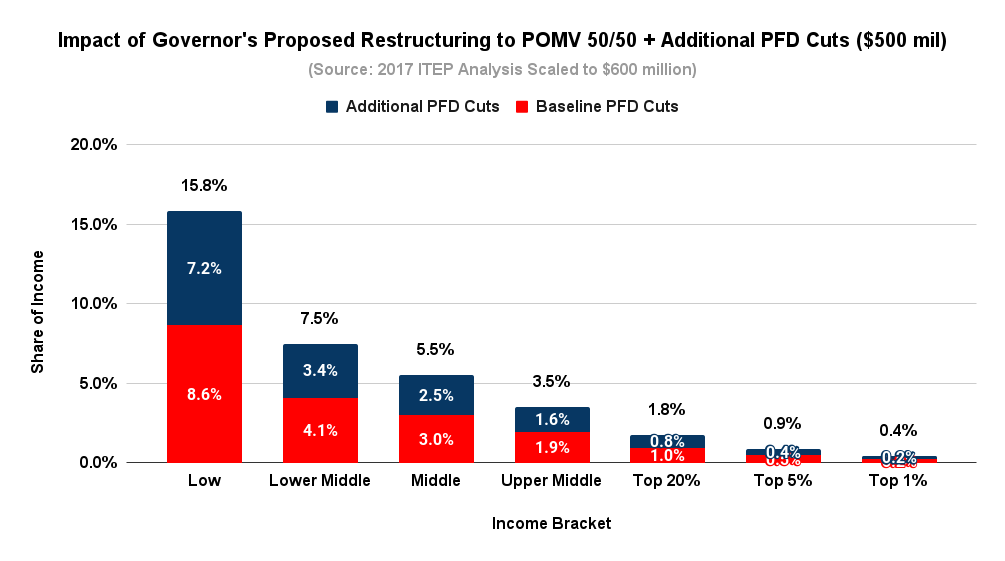

Deeper PFD Cuts. By making the PFD the “leftover” (what’s remaining of the POMV draw after closing the fiscal gap), some propose to close the remaining deficit through additional PFD cuts over and above those already incorporated in the Governor’s proposed baseline.

The cumulative impact on Alaska families of the Governor’s proposed restructuring (in red) and the level of additional PFD cuts – again, “reversibly graduated head taxes” – required to close the remaining gap (in blue) is reflected here:

Because it simply stacks one “reversibly graduated head tax” on top of another, the effective cumulative tax rates follow the same, hugely regressive pattern as the Governor’s proposed baseline, just at much higher levels.

The combined impact results in effective tax rates of 0.4% on the top 1% of Alaska families, 5.5% on middle income Alaska families and 15.8% on the lowest 20% of Alaska families. Looked at in terms of regressivity, the combination takes 40 times more from low, and 14 times more from middle income Alaska families than from the top 1%.

Advertisement. For information about purchasing ads, please click here.

From an economic perspective, the effect is to stack a second dose of the revenue option that has the “largest adverse impact” on the overall Alaska economy on top of the first, in essence doubling down on bad.

Sales Tax. Some propose to close the deficit remaining over and above the Governor’s baseline instead through a sales tax. While some have talked about the “Wyoming” and “South Dakota” approaches, and the Department of Revenue’s November 2021 “Fiscal Plan Model” (DOR Model) allows users to apply something along those lines at a gross level, to our knowledge neither has been analyzed from a distributional perspective.

As a result, as a proxy we have used the distributional analysis of the sales tax included as part of ITEP’s 2017 Report. Because that tax included “exemptions for various necessities such as groceries, health care, prescription drugs, shelter, and child care,” it most resembles the so-called “Wyoming” model, referred to in DOR’s Model as “Mid Base, Exemptions include Groceries, Medical, Fuel.”

As ITEP’s 2017 Report concludes, even with exemptions “general sales taxes tend to be regressive, impacting low- and middle-income families more heavily than high-income families when measured as a percentage of household income. This effect comes about largely because low- and middle-income families spend a larger fraction of their earnings on items subject to sales tax, while high-income families direct a large share of their income into savings and investments.”

We would note that, based on a comparison of the two approaches in a recent, state-by-state ITEP analysis of “Who Pays?” various taxes, the South Dakota approach is even more regressive – would have an even larger adverse impact on Alaska families and the overall economy – than the Wyoming approach.

The cumulative impact on Alaska families of the Governor’s proposed restructuring (in red) and the level of sales tax required to close the remaining gap (in blue) is charted here:

While less regressive than stacking an additional PFD cut on top of the Governor’s proposed baseline, the effective cumulative tax rates nevertheless retain a decidedly regressive slant.

The combined impact results in effective tax rates of 0.6% on the top 1% of Alaska families, 4.5% on middle income Alaska families and 10.8% on the lowest 20% of Alaska families. Looked at in terms of regressivity, the combination takes 18 times more from low, and 7.5 times more from middle income Alaska families than from the top 1%.

Although not as great as PFD cuts, because of their regressive nature, sales taxes nevertheless also have an adverse economic impact compared to other options. As ISER concludes in its 2016 report, because “lower-income Alaskans typically spend a higher share of their income than higher-income Alaskans do … more regressive measures will have a larger adverse effect on expenditures [economic activity].” ISER’s 2017 Report concludes that, after PFD cuts, “sales taxes would be the next costliest for households with children.”

(Progressive) Income Tax. Some propose to close the deficit remaining over and above the Governor’s baseline through a progressive income tax. While some, such as Senator Peter Micciche (R – Soldotna) in a 2017 interview, have objected to a progressive income tax as “unfairly applied” against the state’s higher earners, in our view it’s important before reaching any such conclusions to analyze the combined result on Alaska families of the Governor’s proposed baseline PFD cut and using an income tax to close the remainder of the deficit.

While there have been other, more recently proposed income tax approaches, because it’s the only one we are aware of for which there is a distributional analysis, as a proxy for this review we have used the income tax analyzed as part of the 2017 ITEP Report. That option proposes marginal rates ranging from 0% to 5.075%.

The cumulative impact on Alaska families of the Governor’s proposed restructuring (in red) and the level of income required to close the remaining gap (in blue) is charted here:

Far from Senator Micciche’s fear that such an approach results in tax rates that penalize “higher earners,” the cumulative effective tax rates still retain a regressive slant.

The combined impact results in effective tax rates of 3% on the top 1% of Alaska families, 3.7% on middle income Alaska families and 8.7% on the lowest 20% of Alaska families. While less regressive than either even deeper PFD cuts or a sales tax, the combination still takes nearly 3 times more from low, and 25% (1.25 times) more from middle income Alaska families than from the top 1%.

Because it is the least regressive, as ISER noted in its 2016 Report, of the options it examined “income taxes have the least effect on expenditures [economic activity].”

Flat Tax

As some readers will know, in lieu of PFD cuts or any of the other options, we have long advocated using a flat rate income tax to close Alaska’s fiscal gap remaining after spending cuts have been exhausted.

From a policy perspective we believe such an approach ensures all Alaska families have the same “skin” in paying for government spending levels and, through that, have the same incentive to restrain spending to reasonable levels or, put another way, to find the right balance, collectively, between what Alaskans “want” from government and what they are willing to pay for those “wants.”

From an economic perspective, a flat tax also avoids the adverse impacts resulting from regressive options.

Unlike the other options discussed above, we don’t propose to layer such an approach on top of the Governor’s baseline PFD cuts. As demonstrated by looking at each of the options discussed above, that merely bakes in the regressive tilt of the Governor’s restructured PFD, ensuring that the overall result is regressive as well.

Instead, we propose to replace the Governor’s proposed PFD restructuring and close the entire fiscal gap reflected in the Governor’s FY23 10-year Plan – the $600 million addressed by the Governor’s proposed PFD restructuring and the additional $500 million remaining after that – through a single flat tax.

In analyzing the impact we have used Option 1 – the most flat – of the various alternatives discussed in ITEP’s 2021 report to the Legislature comparing various flat-rate options. As we have noted in previous columns, the Option 1 rate is slightly lower at the lower end of the range than at the upper because it excludes the PFD from the definition of income. That minor difference is correctable by simply including the PFD in the definition of income, the same as is done for federal income tax purposes.

The cumulative impact of using Option 1 to fill the entire $1.1 billion fiscal gap is charted here. The resulting numbers can be compared to the combined results of the alternatives discussed previously.

Rather than the regressivity of any of the other options, the Option 1 flat tax results in an almost uniform effective tax rate across all income levels – 3.2% on the top 1% of Alaska families, 3.0% on middle income Alaska families and 2.4% on the lowest 20% of Alaska families.

Even excluding the PFD from the definition of income, the effective tax rates only differ by 25% between the lowest 20% and top 1% of Alaska families, far from the multiples prevalent under the other options.

And significantly, 60% of Alaska families – middle, lower middle and low – incur lower effective tax rates under this than any other option and another 20% – upper middle income families – incur lower effective tax rates than under the “deeper PFD cuts option” (and roughly the same as they would under the other two options).

Only the top 20% incur materially higher effective tax rates than under the other options, but they aren’t asked to bear any materially higher rates than any other income bracket and their rates are still less than those faced by 60% of Alaska families under all of the other options.

Substitute, Non-Personal Revenue Options

As noted in last week’s column, in addition to enabling users to adjust for various other factors, the DOR Model also allows users to estimate potential revenues available from various other “options,” such as changes to the current oil tax and corporate income tax structures, small increases in the fuel tax, and implementing a state lottery or legalizing casino and video gaming terminals.

A quick summary of some of the options and their estimated annualized revenue over the portion of the 10-year cycle covered by the Model are as follows:

Adopting some (or all) of these revenue options would reduce the need for – and impact of – the personal tax options discussed previously in this column.

For example, according to the DOR Model the state could raise an estimated $130 million by amending the corporate income tax (CIT) to (a) tax digital business activity in Alaska ($70 million), and (b) applying it to pass-through entities (the so-called “Hilcorp fix”) ($60 million). Increasing the motor fuel tax by $.05/gal would raise another $25 million, and layering on the $3/barrel reduction in the current oil tax credit (adjustment) would raise an additional $400 million in substitute revenue.

As we show below, substituting the resulting $550 million for revenue otherwise to be raised, for example, through our proposed flat tax would cut the effective tax rate on middle income Alaska families in half, from 3.0% of 1.5%.

Any revenue package – including even the Governor’s proposed baseline PFD cut – should closely evaluate substituting one or more of these non-personal revenue options for a personal tax on Alaska families.

Conclusion

A realistic look at the state’s fiscal situation makes clear that on its current course, the state is once again facing significant deficits at the other end of the FY23 “bridge year.” To prepare for those, the administration and legislature should use the upcoming “bridge year” to plan and implement a replacement revenue option.

In doing so we believe it is critical that the administration and Legislature focus throughout on the impact of the proposed alternatives on Alaska families and the overall economy. A “sustainable” budget isn’t one that simply matches top line revenues and spending; it is one which also treats all Alaska families equitably and helps support, rather than undermine, the overall Alaska economy.

Brad Keithley is the Managing Director of Alaskans for Sustainable Budgets, a project focused on developing and advocating for economically robust and durable state fiscal policies. You can follow the work of the project on its website, at @AK4SB on Twitter, on its Facebook page or by subscribing to its weekly podcast on Substack.

[ad_2]

Source link Google News